Thursday, April 23, 2009

Just a Question

Have Lenny Dykstra and Beowulf Shaeffer ever been seen together?

Collateral question: Has Jim Cramer ever gotten anything correct?

Labels: baseball, Fraud, High Finance, Jim Cramer, Journamalism, Ponzi schemes

Monday, December 15, 2008

Big Fraud in Little Madison

Earlier in the year I reviewed the investments held by the Madison Cultural Arts District's trust fund, which once had been intended to use stock market returns (and later alternative investment returns) to pay the Overture Center's construction debt and contribute to the Center's operations. I concluded that the fund was undercapitalized and needed to get cracking on fundraising. In September, the fund reached a point where it was to be liquidated to pay off the bulk of the construction debt, leaving the major donor and the city of Madison on the hook for the balance. We only recently, as lapsed Madison Symphony subscribers, received a fundraising letter.

An interesting detail is that when I'd reviewed the MCAD trust's assets, it held $17.9 million — just under 18 percent of its $100M portfolio of the time, in the Fairfield Sentry fund. (In early '06, they had an even greater exposure.) At the time, Fairfield Sentry was among the trust's high-flying investments, relatively speaking. I said "who knows" with respect to how Fairfield found its alpha.

Well now we know! Per Bloomberg (via), Fairfield Sentry was 100% invested in Bernard Madoff's mega-swindle! I hope they actually managed to liquidate their balance. If they did get out soon enough, then at least the MCAD trust may not have been the biggest of suckers in one respect.

Otherwise, big potential losers are Andrew Ang, Matthew Rhodes-Kropf, and Rui Zhao, whose April '08 NBER working paper concluded that funds-of-funds "on average, deserve their fees-on-fees." At a minimum, they should delete the Madoff suckers and recalculate.

Labels: hedge funds, High Finance, Madison

Tuesday, April 29, 2008

Glories of the Working Life (first of a series)

Ignore, for the moment, the presentation values that were quite acceptable fifteen years ago (i.e., that it looks as if it was prepared in MultiMate or WP 5.1 with Helvetica).

Note the boxed entry.

Users may also wish to examine how many of the presenting firms are still intact in their present form.

Labels: fragments of the past, High Finance, just life

Friday, April 11, 2008

Overture Center Finances: A Fine Mess

Quick background: The Overture Center, Madison's $205 million concert hall and arts center, was a gift from local philanthropist Jerry Frautschi (who made his fortune investing in American Girl, founded by his wife and sold for big $$ to Mattel). The gift was structured so that about half was put in a trust fund, intended to pay off construction debt and contribute to the Center's maintenance, assuming it made roughly 9% annual returns off stock market investments. The year was 1999. D'ohh!

After years of 2% annual returns, the trust fund represented insufficient collateral for the bankers, so a refinancing plan was hatched, and approved in late 2005, that required the City of Madison to guarantee a portion of the debt. The plan would work just great as long as it attained an 8.25% annual average return and the trust balance stayed over $104 million. That also hasn't worked out so well, as noted here a week-and-a-half ago.

My question has been, how have the Overture trust fund's managers managed to screw up so badly? Well, other than the obvious reason that 8.25% is well above any sane person's idea of a risk-free return. Courtesy of Isthmus executive editor Marc Eisen, I've seen a spreadsheet with a summary of the Overture trust's investments, and can only conclude that the investment choices never gave them a serious chance. For junkies of mid-sized institutional asset management stories, some gruesome details are after the jump.

I'd divide the trust fund's management into two eras, the Cash Era and the Alternative Investments Era.

The Cash Era ran from late 2005 to late 2006. The trust fund's balance ranged from $106.2 million to $109.3 million over the period, and 46% to 61% of that was held in "cash equivalents." The balance was in "general equities" (which I take to be meant generically, and not the firm General Equities) and Fairfield Sentry Ltd., a hedge fund. The higher cash percentage was sustained for the latter two-thirds of the year, when the trust turned a good portion of its Fairfield Sentry holdings into cash equivalents. My naive calculation from the spreasheet says that the equitites returned 4.6% and the Fairfield Sentry fund returned 8%. In 2006, you could have made right around 5% with a very good money market fund, such as the institutional share class for Vanguard's Prime Money Market fund. The upshot was that their weighted average return was right around 5% for the year. With that asset weighting, the trust had to make 12.7% off the non-cash-equivalent assets to reach the 8.25% target. 2006 actually was a good year for stocks — Vanguard's Total Stock Market index fund returned north of 15%. They chose a bad year not to be 'seeking beta.'

The interesting question is why they stayed in cash for so long post-refinancing. Pardon me for thinking that the financial geniuses behind the refinancing might have had an investment plan ready to roll upon approval. None of the obvious answers — they didn't have a plan, the Cash Era represents an inept plan, and they chose a deliberately defensive position to avoid the political embarrassment of a quick I-told-you-so from refinancing opponents — is confidence-inspiring.

The Cash Era ended in late-2006, as the cash-equivalents gradually moved into a series of other investments. At the end of the series I've seen (3/14/08), only 2% of the Overture trust is held in cash equivalents. I call this the Alternative Investment era as it was kicked off with a roughly $15M investment in "Highbridge Fund," which appears from the value of holdings to be the quasi-hedgey Highbridge Statistical Market Neutral fund (as of 3/14, 21% of the fund's holdings). Stakes in Pimco All Asset fund (a fund of Pimco funds, 16%), principal protected notes (PPNs) from JPMorgan and Barclay's (the latter purchased with the proceeds of the "general equities,"14% and 8%, respectively), additional investment in Fairfield Sentry (18%), and "JPMorgan muni's" (20%) followed.

It's hard to reliably track performance across the board because of apparent asset sales and purchases, but nothing has come especially close to putting in an 8.25% return over the period. The highest-flyers, the Fairfield and Pimco funds, have had 1-year returns around 6%. The Highbridge 1-year return was 1.2% (they've done relatively well YTD), the munis are up 2% over the 7-month period they've been held, and the PPNs down. The upshot is that the trust is showing a weighted average return around 3% for the last year, far below the target. Granted, all I need to do is look at my 401(k) performance to see that it's been a tough year through the end of March — I'm down 3.3%, though then again my five-year average is 9.7%. An irony is that while Madison Cultural Arts District Treasurer told the Cap Times that it would be "a very unfortunate change" if the creditors forced the assets into Treasury securities, which might be true now, had they actually been in Treasurys all along, they'd have ridden the bond market's flight to quality well past their return goal for the past year. Whatever the skills of the MCAD, investment timing ain't it.

The better question, perhaps, is what the prospects would be for this asset mix to earn 8.25% on average in the future. The underlying assets for the PPNs could be anything, so it's hard to say there. The munis won't under foreseeable interest rate environments. Pimco All Asset seems to be tuned to produce single-digit annual returns. Highbridge hasn't exactly been minting 'alpha,' and who knows about Fairfield Sentry. If the PPN investments were selected at least for perceived safety before the fact (actual performance notwithstanding), then I'd have to say it isn't going to happen. If nothing else, the MCAD seems to have done a good job of picking relatively high-cost holdings, which just increases the return that has to be earned from the underlying assets for the trust to net 8.25%.

This brings me back to my main point — the MCAD is undercapitalized, and they should get cracking on raising money. That was something that was supposed to have been facilitated by keeping the facility in the hands of the MCAD instead of under direct city ownership, but a capital campaign seems to have become a priority only now that they're in the soup. If they want to make good on the facility's promises, and shut us critics of their financing misadventures up, they need to raise a lot.

Return to the Marginal Utility main page.

Labels: hedge funds, High Finance, Madison

Thursday, April 03, 2008

In the Meantime, We are Reminded what the phrase "Representative Government" Means

I'm watching (mercifully, with the sound off) Christopher Cox (R-CA; patronage job as SEC Chairman), if CNBC is correct, blatantly lie to Congress (CNBC Chyron: "What happened to Bear Stearns was unprecedented" Let's see: a major financial player with large bets in a specific market sector gets caught ignoring the rule "The market can stay irrational longer than you can stay liquid." Where have we heard that before?) and figuring that Yves or Steve Randy Waldman will take care of it so I don't have to.

And I start fearing for the democratic process, because seeing Christopher Cox explaining financial markets as if he knows anything about them other than how to provide patronage is scary.

So it is reassuring to see this piece on Political Radar, as a reminder of that vox populi does, occasionally, work:

In the Senate this week, a bipartisan bill to help stem the tide of foreclosures nationwide is sliding through the senate like water on Teflon.

A similar bill fell prey to partisan bickering at the end of February when Republicans blocked it after Democrats refused to allow unrelated amendments.

What happened between then and now to end the partisanship? Vacation. That's what. Because while most people take vacation to forget about their jobs, in Congress they take vacation to go talk to their bosses, the people.

"I suspect the other major event was the fact we went home for a couple of weeks. Nothing like going home, Mr.. president, to get a message," said Sen. Chris Dodd, the chairman of the Senate Banking Committee, who engineered the bipartisan bill in a marathon 20 hour bipartisan brainstorming session with Sen. Richard Shelby, R-Ala....

"But they asked the legitimate question, if it was good enough for people to get together to solve a problem on Wall Street, what about the problem on my street? What are you doing here to see to it I can stay in my home? That our neighborhood will not collapse? That our taxes and properties and neighborhoods will not further deteriorate? I suspect more than anything else, going homemade a big difference and -- going home made a big difference."

In the world of economists, this will probably be seen as an inefficient solution, encouraging the (mythical) Moral Hazard.

But in the real world, Congress has ready access to Wall Street bailout advocates. It's only on vacation that they speak with the people who elect them.

It appears that Gore Vidal is correct that the Congressional offices and buildings should never have been fitted with air conditioning: not because of the mischief-making, but rather because it reduces the chance of their getting actual voter input.

Labels: Democracy, High Finance, Moral Hazard, Regulation, The Old Firm

Wednesday, April 02, 2008

Even I'm Not that Gullible

Metro reported yesterday that CBS's Les Moonves was so impressed by Britney Spears's appearance on How I Met Your Mother that they decided to make her the centerpiece of a show—a remake of the Mary Tyler Moore Show.

It wasn't until I read the link at this post from Steve Gould of EoB that I realized that yesterday was more than the traditional birthday of our cat.*

So I'm gullible. But even I'm not as gullible enough to believe the claim of Lehmann's CEO today that he has evidence that hedge funds "conspired" to destroy Bear Stearns by short-selling.

It's not that I don't believe multiple hedge funds shorted the firm, or even that some of them spoke with each other. But the conversation was more likely,"Are you short BSC?" "Better believe it. You too?" "Of course." than some clandestine activity.

Let's be clear: when your firm is leveraged over 30x itself, when most of your revenues come from an area that hasn't generated enough volume to support your structure in over a year (even after two major rounds of layoffs), and when your swap spreads blow out by a factor of 15 or 20 in the course of a few weeks, short sellers (who have to risk a lot more capital than derivatives traders) are the least of your concerns. Or just the icing on the cake.

Mark Gilbert mostly gets it right here:

U.S. and U.K. regulators are wasting their time threatening traders who profit from speculation about the deteriorating health of the financial community. The gossips aren't to blame for the demise of Bear Stearns Cos., and they won't be at fault when the next firm goes bang, either.

Brokers, futures traders, collateral managers and compliance officers are ranking their counterparties from strongest to weakest, and choosing to stop doing business with whichever company comes bottom. If the same name gets crossed out on every list, it spells game over for the loser -- deserved or not.

And, to be clear, when you have done Jack about it in the month leading up to the day before Ben Bernanke decides he needs to help you because no one else will, two dollars a share is for the other shareholders; getting punched out in the gym (note the correction at 7:53a.m. on 3/28) is Getting Off Easy.

But the seeds of Alan Schwartz's destruction-by-inaction were, as Gilbert notes, planted in 1998:

In his 2001 book When Genius Failed, Roger Lowenstein details the Fed's crucial 1998 meeting to convince Wall Street that it should shoulder the financial burden of keeping Long-Term Capital Management LP afloat or risk financial meltdown.

James Cayne, the CEO of Bear Stearns, told his peers—including Philip Purcell of Morgan Stanley and Herbert Allison of Merrill Lynch—that his company wouldn't join the 14 securities firms paying for the rescue.

"In unison, the CEOs demanded an explanation," Lowenstein writes. "This only made Cayne more resolute. Bear had enough exposure as a clearing agent, Cayne said. He wouldn't say more. Suddenly these paragons of individual enterprise seethed with communitarian fervor. Purcell of Morgan Stanley turned beet red. He fumed, 'It's not acceptable that a major Wall Street firm isn't participating!' It was as if Bear were breaking a silent code; it would pay a price in the future, Allison vowed."

Only the Stevens Levitt and Dubner might be surprised by that reaction. The rest of us noticed that, when rumors of an illiquid Lehmann started spreading, the first thing that happened was that Goldman Sachs trotted out a Senior Executive to confirm that they view Lehmann as (something like) "a strong, viable competitor."

When rumors started about Bear, there was about three days of silence, followed by the negotiations of March 14-16 to avoid Chapter 11 on the 17th.

That may be a case of revenge being a dish best served cold. Maybe the calls were made and no one was willing to do what Goldman did for Lehmann.

But all of the other evidence is that upper management just didn't realise that its job isn't to manage departments so much as to manage public perception by making certain that anything that might worry investors—say, the market for your CDS swap spreads going well past junk levels—is handled quickly and publicly.

That's why they pay the CEO—and the Board of Directors—the big bucks and bigger stock options. In early March, several "leaders" of BSC proved they were overpriced.

*No picture, in keeping with this plea.

Labels: hedge funds, High Finance, leverage, liquidity, The Old Firm

Don't Say You Didn't Get Anything From the Bailout

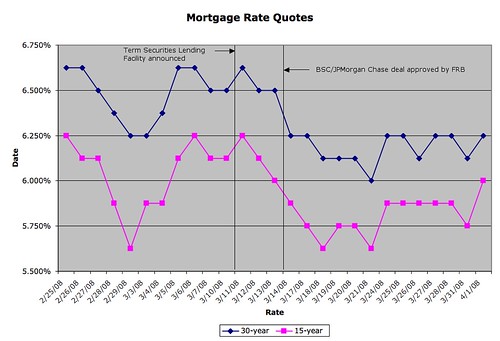

Here's another update to a recent post, in which I sought to figure out what was in the recent efforts by out monetary policymakers to deal with the housing troubles for me — relatively responsible borrower who still (probably) has a fair amount of home equity. Initially, the answer seemed to be Sod All, but that's changed a little, as you can see from the updated graph:

I've shown the FRB announcements of the Term Securities Lending Facility and of the approval of the BSC/JPMorgan Chase deal. Particularly after the latter, the 30-year rates (on a zero-point cash-out refi with 80% LTV) appear to have dropped around 37.5 bp from the previous range; let's call the sustained drop for someone who can afford a 15-year amortization 25 bp. So there's a little something for Main Street, though these rates aren't near the historic lows that are sometimes credited as a "fundamental" factor behind the house price run-up (in my not-so-extended family, there's at least one 15-year mortgage where the first digit of the rate is a 4).

Whether this will turn out to be worth more to the public than MBS losses flowing through the Fed to the Treasury remains to be seen.

Labels: High Finance, monetary policy, Personal Finance Advice of Alan Greenspan

Tuesday, April 01, 2008

Some Reality Reaches Our 70 Square Miles

1. Hilldale Phase 2 delayed (again), a little sign of the CRE bust?

Barry Adams's State Journal lede blames the "harsh winter and changes to the design" for a delay in the start of construction at the seven-acre moonscape across from the office until July. This would house a greatly expanded Whole Foods, provide 3 floors of office space, and a 140-room hotel. When last we heard from Jos. Freed & Co., just a month ago, the harsh winter, the phase was supposed to be completed by spring to summer '09; it's now fall '09 to early '10.

I'd figured that Whole Foods would keep the project more-or-less on track, especially seeing as there's reportedly a tenant interested in a full floor of the office building. Oh well.

This project had been an example of the condo bust's losses looking like CRE's gains, at least for a while; the hotel replaced one proposed condo tower, and another mixed-use building (3 floors of office, eight of condos) was scaled back to a 5-story office building, since reduced to 3. Next stop, the soccer fields at Hilldale Phase 2?

2. Big Sh*tpile in Little Madison Revisited, Overture trust balance reaches new lows.

Who could have predicted that 8.25% annual returns aren't risk-free? Well, Mayor Dave Cieslewicz, of course, and the editorial pages of both papers.

The geniuses who manage the trust's investments have managed to turn $109.3M in December '05 to $100.1M as of March 14; they needed to maintain $104 million to make the 2005 refinancing work as advertised, with the trust paying the construction debt and making a contribution to the Overture Center's maintenance.

The problem has been pretty simple all along: too little money required to do too much stuff, so the plan has depended on generating returns sufficiently large that they can't be counted on all the time. As it turns out, you can be too generous and too cheap. The original assumption was a 9% annual return (in 1999, when it was assumed it would be generated from stock market holdings), and the times being what they are, they got 2% through 2005. The refinancing plan shaved off 75 bp, but was especially sensitive to low realized returns in the early years (oops).

Something I wonder is why a nonprofit endowment like this can't buy into a better class of money management. Some of you have surely seen that the peer group for Jane Mendillo, the Wellesley investment manager recently hired to helm the management of Harvard's endowment, turned in a 13.9% 5-year annual average return to the middle of last year. (I'm curious to see what the last nine months have done to the high-flying endowments.) The Overture fund isn't in this size class, but nevertheless I wonder how its management does so poorly? And why can't they just buy into the competent management of larger endowments (i.e., are there tax or regulatory obstacles to doing so)?

The solution, of course, is to raise more capital for the fund — something that was advertised as being facilitated by retaining quasi-private ownership of the facility, but which has yet to materialize except, perhaps, by way of a bailout to prevent a chorus of I-told-you-sos.

Labels: High Finance, Housing Bubble, Madison

Friday, March 28, 2008

The Perfect Negative Indicator?

Jim Cramer's column in Metro this morning was singing the praises of Toll Brothers and Ryland, another homebuilder. So it is probably only right that CR finds this:

The little bit of good news was KB Home's cancellation rate improved slightly (similar to other builders):

The Company’s cancellation rate improved to 53% in the first quarter of 2008 compared to 58% in the fourth quarter of 2007.

After his BSC call, I didn't think there was anywhere else for him to go. But clearly he's "Workin' in a Coal Mine":

Workin' in a coal mine

Goin' down down down

Workin' in a coal mine

Whop! about to slip down

Added: A Yahoo! Finance graphic for the optimists who think there may be more to Residential Housing than the general market:

Just for giggles, here's the three builders, over the past year, vs. the S&P500 Index:

UPDATE: My Loyal Reader, whose sense of time comes from a Mark Thoma link, recommends "the original" video.

Labels: High Finance, Housing Bubble, Journamalism

Thursday, March 27, 2008

Jimmy Cayne Cashes Out

...for $61.3 million, sez the AP. (That's 5.66M shares at $10.84 each.) Nice work if you can get it.

Labels: High Finance

Tuesday, March 25, 2008

The Price Increase: a BS violation, but maybe with a purpose

I've been trying to figure out the

As Carney notes, many of us who said nothing at the $2 level are screaming Bailout at the four-fold increase.* (Tom and cactus, as I noted yesterday, were ahead of the curve—I still think they were wrong, but let's go with prescient.) And, to give him credit, he also notes that this (1) may have been necessary for the market and (2) the shareholders could still make a lot of trouble (if they're as

Let us think for a minute about Black-Scholes. One of the key elements of the model is that square root of time thing: the longer you have to expiry, the higher the time value of the option.**

JPMC just went from having a lock-in until March of 2009 to needing things to be done on 8 April 2008. And they're paying more.

But, to reference another former firm,*** there was a period of time—around mid-2000, iirc—where Carly Fiorina (whose leadership and management skills are legendary) got it into her head to buy the consulting arm of PwC for about $18 billion. And negotiations went on and on. Others from the HP side talked it down to about $11 billion, and then HP decided that the employee turnover rate (the best of the Big Five, but still twice what HP was used to seeing) was too high. So the deal was called off.

For the six or seven months of that roundelay, though, the senior partners of PwC did virtually no Business Development. (Exceptions noted, but they were exceptions.) They were, as it were, counting their money.

So by the time the deal fell apart, the pipeline was dry. And along came a recession, and then 11 Sep 2001, and finally the business was sold to IBM in mid-to-late 2002 for, iirc, $3 billion.**** (HP went out and found a company with a low turnover ratio—Compaq—and the synergies created there made it a powerhouse that has only added to Ms. Fiorina's reputation.*****)

Now, I'm not saying that the time spent on the failed HP merger drained between 75 and 83% of the value of the company—but there's a reasonable argument that the market did, and it is certainly true that distracted partners don't generate the revenue stream that dedicated ones do.******

Now think about that in the context of an investment bank, where the cash flows are larger, quicker, and more fleeting. A business idea that is six months old still has value. A trading algorithm that gets delayed six months is likely to lead to losses.

So I suspect believe that Jamie Dimon has just played the last trump: "You want another $1 billion for the equity holders? All right, but you've got to finalize the agreement on this deal in the next two weeks, or I'm taking your building. And, by the way, if the deal fails, the market has already smelled blood twice. So Bring It On, if you want. But be careful what you wish for; you may get it."

Whether he finished with "Do you feel lucky, punk?" is left as an exercise to the reader. But with the value of the assets declining daily, Dimon probably realised that Black-Scholes wasn't the model to use for valuation.

It's still a bailout, but it appear to have a working logic to it.

*Yes, I said four- not five-, fold. Round figures, the swap went from 0.05 JPMC shares per BSC share to 0.21 shares, which is just over a four-fold increase (ca. 320%). The rest of the appreciation came from the rise in JPMC's stock.

**It's also one of the reasons no one would ever use the standard model to price a long-dated option. But that's a sidebar, not relevant to the example at hand.

***I've got a million of them. Well, sometimes it feels that way.

****None of these numbers or dates is necessarily accurate, but I believe they're close. You can look them up.

*****This you can definitely look up.

******It was legend at Bear that one of the then-current Compensation Committee members had maneuvered his nearest rival out of the job when the latter was tending to his cancer-stricken wife. But again I digress.

Labels: financetheory, High Finance, Moral Hazard, The Old Firm

The Moral Hazard Contagion Spreads

Tanta notes that Wells Fargo is begging, which they weren't doing when the BSC price was $2/share.

Yes, the plural of anecdote is not data, but the timing here is not coincident.

More later.

UPDATE: I see cactus at AngryBear is thinking the same way, though rather more like an economist than a taxpayer.

Labels: bankruptcy, High Finance, Moral Hazard, The Old Firm

Friday, March 21, 2008

A Fate Worse Than A Fate Worse Than Death

Cheers to Angry Bear's Cactus for pushing back against the meme that the near-wipeout of Bear Stearns shareholders means that there wasn't a bailout on. (For an example, hear Laurence Meyer in this NPR segment, which for the record starts with possibly the worst explanation ever of the origins of the present crisis from reporter Adam Davidson. [*])

On a maybe related note, I was scratching my head over the NYT editorial board's observation that:

[I]f the objective is to encourage prudent banking and keep Wall Street’s wizards from periodically driving financial markets over the cliff, it is imperative to devise a remuneration system for bankers that puts more of their skin in the game.Oh really? Whether or not it was enough, Jimmy Cayne experienced a 9-figure paper loss last weekend. The LTCM partners' large share of the fund's equity didn't stop them from almost blowing up the markets.

[*] See here for explanation. Also please keep in mind the cultural subtext of the "worst X ever" formulation.

Labels: High Finance, The Old Firm

Thursday, March 20, 2008

And You, Sir, Are No Genius

The last few nights, I've been enjoying Roger Lowenstein's When Genius Failed: The Rise and Fall of Long-Term Capital Management. At least, I've been marveling at its parallels with the present crisis — not principally because of JM's latest round — in-between thinking that I might sleep better were I reading "Call of Cthulhu" as a chaser to a late-night screening of Alien.

The density of Famous Last Words and Unheeded Cautionary Lessons is too high as to make a comprehensive review possible (yet 'nobody' saw the current crisis coming), but here are a few favorites:

Removal of these financing constraints [margin rules] would promote the safety and soundness of broker-dealers by permitting more financing alternatives and hence more effective liquidity management... In the case of broker-dealers, the Federal Reserve Board sees no public policy purpose in overseeing their securities credit.That's Alan Greenspan, testifying to Congress in 1995.

[Fama] argued that Black Monday had been a rational adjustment to a (one-day?) change in underlying corporate values. On the other hand, Lawrence Summers... told the Wall Street Journal after the crash, "The efficient market hypothesis is the most remarkable error in the history of economic theory." (p. 74)And that's saying something?!

Almost imperceptibly, the Street had bought into a massive faith game, in which each bank had become knitted to its neighbor through a web of contractual obligations requiring little or no down payment... "Credit limits for customers are an essential tool for credit risk management," [The New York Fed] warned. [emphasis in original]Shockingly, the warning was in a letter to Wall Street banks, not business undergrads.

Writing in the prestigious Journal of Finance, Andrei Shleifer of Harvard and Robert W. Vishny of Chicago presciently warned that an arbitrage firm of Long-Term's type could be overwhelmed if "noise traders" pushed prices away from true value... [T]hey predicted that, in such a case, arbitrageurs would "experience an adverse price shock" and be forced to liquidate at market lows. Merton... pooh-poohed the notion that markets could be overwhelmed. (p. 111)

Merrill's willingness to finance its client was part of a pervasive climate of financial laxity, palpable in Wall Street's eagerness to underwrite emerging markets. (p. 130)Let's play "substitute the asset category!

The comforting notion that global financial cops would always be there to put matters right was now exposed as a fallacy. This time, there was no rescue by the IMF, no hurried bailout by Robert Rubin or the Group of Seven Western powers... It "punctured a moral hazard bubble" that had been inflating expectations... Investors, at first singly and then en masse, concluded that no emerging market was safe. In seventy years, Russia's Communists had not succeeded in dealing markets such a telling blow as did its deadbeat capitalists. (p. 144)

Most of us survived 1998, but we'll see if our deadbeat capitalists can one-up their Russian counterparts...

Labels: hedge funds, High Finance, Personal Finance Advice of Alan Greenspan

Wednesday, March 19, 2008

Bear Investors bet that Moral Hazard Doesn't Exist for Them

The Wall Street Journal has several articles today on the death of The Old Firm. Most interesting is "Heard on the Street" (link requires sub), where investors appear to have decided to play a game of Chicken with both Jamie Dimon and the Federal Reserve.

There will be a lot of noise about this over the next few months, and someone (not me) will get a nice dissertation out of the results.

Most interesting, though, from an asymmetrical information point of view, is this one, which notes that the inept Christopher Cox-led (but I repeat myself) SEC:

issued a written statement suggesting it has expanded an inquiry into Bear Stearns Cos. to include what was or wasn't said in the two months leading up to the brokerage firm's unraveling.

The SEC, which is usually mum about investigations, said its enforcement division wrote a letter as J.P. Morgan Chase & Co. was negotiating to take over Bear. The letter addressed to J.P. Morgan concerned "investigations and potential future inquiries into conduct and statements by Bear Stearns before the public announcement of the transaction with J.P. Morgan."

The Bear speculators are treating the stock as if it were SCO, which for a few years was basically a gamble on a successful lawsuit. That effort has not been pretty.

Strangely, their greatest hope may also be their greatest weakness, renowned bridge player and former CEO Jimmy Cayne. As the New York Post notes:

Cayne, who is a member of Bear's board of directors and voted for the JPMorgan deal, could risk further embarrassment if he threatens to vote against the deal, sources said.

The "I was for it before I was against it" strategy is not something I want to gamble $4/share on. Your taste for lawsuits may vary—just be certain they are suits in your favor, not against you.

Labels: High Finance, Moral Hazard, The Old Firm

Sunday, March 16, 2008

Profit Sharing -- Not even at 1992 prices

Iirc, and I probably don't, the first time I got BSC stock options was during my first go-round there. They were around $50/share, which was a minor premium when issued and a discount by the next year.

This time, for once, it appears the Fed did its job: tried to save the market, not the malfeasant firm.

But $2 a share is brutal. At that level, even Jamie Dimon and the crack

It's always been especially true at BSC that the assets walk out the door at the end of the day. The question now is how many of them will bother to walk in the door on Monday.

The counterpoint, somewhat, is offered by Steven Randy Waldmann, citing the always worth reading jck of Alea, while Mish suggests that derivatives may be a major issue, which is possible but unlikely, save in the balance between long- and short-term assets.

But after Carlyle got squeezed, and now BSC has fallen, it seems fair to ask exactly what the purpose of the TSLF is.

Unless, of course, you assume that market participants are using the three weeks (now 11 days) before it starts to kill of some competition. And no one in the financial services industry would do that, would they?

Labels: FRBOperations, High Finance, Moral Hazard, nce, The Old Firm

Am I Missing Something?

A theme that's going around (for good reason) is that the serial Fed bailouts are a form of covert nationalization of the financial system. It strikes me that an important distinction between the current goings-on and a canonical nationalization is that the Fed's term lending facilities allow the taxpayer to take on risk via the possibly radioactive assets move to the Fed's balance sheet without capturing any proceeds of re-privatization. Indeed, it doesn't even seem that the public even stands to collect a moral hazard-compensating penalty interest rate. (To be clear, my concern here is with how the public is compensated for the bailout, not with the bailout per se.)

Since the Republicans presiding over what otherwise looks like the demise of postmodern financial capitalism are trying hard to forestall what may be less friendly public interventions — witness the WPE warning about overcorrection — this seems to be considered a feature rather than a bug.

So what am I missing?

Labels: High Finance

Saturday, March 15, 2008

Helicopter Ben vs. the Black Swan

Ken probably should write this post from the perspective of someone who isn't necessarily just playing armchair analyst. But here goes anyway.

Brad DeLong figured that the assumption that the Fed wasn't going to allow BSC to fail would be a buy signal: a play on the Fed's willingness to accommodate moral hazard. "Mr. Market" disagreed.

My guess is that Brad is right that there's a moral hazard premium, but that it was swamped by the discount for Mr. Market having failed to put a price on BSC that appropriately reflected the possibility that but for yesterday's intervention it would have collapsed if not yesterday then imminently.

As Dean Baker repeatedly tells us, elite opinion has been busy soft-pedaling the crisis all along. The possibility can't be eliminated that elite opinion believes its own bullshit, at least to some extent. (Just about every recent rally seems to have been on news [i.e., large unconventional Fed interventions] that has had at least a subtext of "things are much worse than they seem, even after accounting for the fact that things are much worse than they seem," to borrow a DeLong-ism.) That would make things rife for Wile E. Coyote past the cliff edge corrections.

Labels: High Finance

Friday, March 14, 2008

It Really IS time to move my 401(k)

Via Felix, a short, sharp shock:

With the support of the Federal Reserve Bank of New York, JPMorgan said in a statement that it had “agreed to provide secured funding to Bear Stearns, as necessary, for an initial period of up to 28 days.”

For the next month, JPMorgan will work with Bear Stearns to reach a solution for its financing crisis. Options could include organizing permanent financing or, according to people briefed on the discussions, buying the bank for a discounted price.

“JPMorgan Chase is working closely with Bear Stearns on securing permanent financing or other alternatives for the company,” JPMorgan said in its statement.

And that's the good news.

Now, let us translate:

In a statement issued on Friday, [Bear’s chief executive, Alan Schwartz] said: “Bear Stearns has been the subject of a multitude of market rumors regarding our liquidity.

People have noticed that our CDS spreads are higher than Argentine debt ca. 2001.

We have tried to confront and dispel these rumors and parse fact from fiction.

To do this, we enlisted Margaret Seltzer, who came highly recommended by James Frey.

Nevertheless, amidst this market chatter, our liquidity position in the last 24 hours had significantly deteriorated.

Nobody believed me on CNBC yesterday; my e-mail has been filled with "The truth will set you free."

We took this important step

We threw ourselves on the mercy of the Fed and JPMC, which may do for us what BofA's support has done for Countrywide.*

to restore confidence in us in the marketplace, strengthen our liquidity and allow us to continue normal operations.”

In the desperate hope that, since Jimmy's gone, the people who remember that we kept all the LTCM collateral for ourselves will be nicer to us than he was to them.

*Insert your own Eliot Spitzer/Jessica Cutler joke here

Labels: credit, High Finance, liquidity, The Old Firm

Thursday, March 13, 2008

Krusty is Coming?

Ripped from today's headlines...

Isn't it amazing how — amid all these signs of the economy headed down the toilet — the indefatigable Wall Streeters can reportedly find solace in the predictions of a firm which, in the most charitable reading, was blindsided by the need for the asset write-downs to date.

Dean Baker will, no doubt, find endless blog material among people who somehow managed not to see the commercial real estate crash coming.

Labels: High Finance, Journamalism

![]()