Wednesday, April 30, 2008

In Search Of Sensible Transportation Policy

Rant time!

I write not to bury Hillary Clinton for joining Chickenshit [*] John McCain's Gas Tax Pandering Express [**], even though she's full of it and Barack Obama is on the side of the angels. Nor do I intend to put my Dean Baker hat on in saying that even this Washington Post debunking fails to note that Obama is right that the hypothetical maximum "gift" [***] to someone who drove 3,500 miles over three months at 20 MPG would be on the order of $30. The Economists for Obama have a nice graph showing why even this is wildly optimistic. Moreover, $30 is all but rounding error in the chickenshit 'economic stimulus' payments [****], which as bright a light as George W. Bush says is in part intended as compensation for high fuel prices. I'm also inclined to deny Hillary's grab for an additional populist point for being willing to tax oil companies to pay for the gas tax holiday, since we all know what the chance such a provision would have of passing a Republican filibuster in the Senate is.

Returning to yesterday's QOTD, a question for gas-tax repeal advocates would be whether they think gas prices are "too high" by only 18.4 cents. Even rolling prices back by $1 would only be to slow the rate with which particularly auto-exposed exurbanites are getting boiled in oil. I imagine that an enterprising reporter who asked Chickenshit John or HRC why we shouldn't be subsidizing gasoline would be told (correctly) that such a thing would be madness, but you can't derive that from the fuel-affordability rhetoric.

Also largely absent from the discussion, and highlighting its essential bogusness, is any mention of structural changes to the U.S. transportation system. The Obama campaign at least devotes a paragraph to the proposition that our transportation needs go beyond greener automobiles; that's one more than HRC. Chickenshit John, who you may recall recently gained plaudits from the press for ditching his wife's jet for the Acela Express, is a famous campaigner against operating subsidies for passenger rail — subsidies which, thanks to the external costs of the alternatives, actually can make more than a little economic sense.

Substantially rebuilding the transportation system requires a lot of time and money (plus maybe some NIMBY arm-twisting), putting the project in need of early and strong political support. (The money, at least, could be obtained largely by ending the most useless parts of the DAMN WAR.) Trying to counteract the price signal that's telling us that we should reconsider the easy motoring lifestyle is worse than doing nothing.

[*] Certain elements of the left blogiverse have taken to calling McCain "Saint John" after the candidate's inability to do wrong in the eyes of the Washington press corps. Irony is dead, people! Gail Collins, who's been pretty good on the subject of late, writes:

[McCain] is fearless when it comes to delivering unpleasant news to people who are probably not going to vote for him anyway.No reason not to say what we really think, eh?

[**] Making members of the Pigovian Tax Club cry since April, 2008!

[***] I.e., assuming the full incidence of the gas tax is on consumers and not, at least in part,

on producers and/or distributors.

[****] As Grampa Simpson might say, I didn't ask for it, don't need it, but gimme gimme gimme!

Labels: Economics, Energy, Vituperation

Tuesday, April 29, 2008

My inbox begs for money

While I just described giving money to move Gary Farber from a good city to an all-right city as a good idea, I can't get such enthusiasm for the latest mailing, which seems to be from one of those Nigerian businessmen, except it lacks their usual verve, charm, and, yes, even style:

Today, there are 47 million uninsured individuals in the U.S., and nearly a quarter of them are children. High costs and limited access are the underlying, fundamental problems in our healthcare system.

Separate thoughts in the same paragraph, not for the last time. This reveals that the writer is not a native English speaker.

As you know, both Senators Hillary Clinton and Barack Obama are touting outrageously expensive and unrealistic universal health care plans - a government monopoly over health care.

As is common knowledge, I wish that were so in the case of Obama. Again, confusing monopoly and monopsony gives away the game. Either Nigerian or a Friend of McMegan (link is not to a friend of McMegan, but rather to someone whose work you should be reading).

Unlike my opponents, I do not believe that all of our nation's problems can be solved by turning control over to our government, with all the tax increases, new mandates and government regulation that come with that idea.

Unlike the current system, where tax increases, new mandates, and government regulation that come with no idea. I'm starting to lean toward FoMcM, since no Nigerian ever talks about being regulated. Thought that "opponents" thing does imply some Civil War.

Today, our campaign began running a television ad focused on health care...to ensure all Americans hear the truth about how I plan to tackle the challenges facing our nation's health care system. To ensure this important ad is aired in as many markets as possible, I'm asking for your immediate financial assistance.

Ah! There it is! The pitch is just where the Nigerians put it.

I believe the key to real reform is to restore control over our health care system to the patients themselves. Americans need new choices beyond those offered in employment-based coverage.

The last time the "the patients themselves" had "control" over their part of the health care system was before Arizona was a state. Most "hospital" care was provided by charity wards run by churches.

This e-mail may not be from a Nigerian, but it's clearly from someone who wants to turn out health care system into the Nigerian one.

My friends, this is not my definition of real reform. I hope you will join me in my fight to tackle the real problems facing our nation's health care system by making a contribution of $50, $100, $250, $500, $1,000, or $2,300 to help fund this important ad.

There's the pitch again. But...$2,300??? That seems small for a Nigerian.

I hope to hear from you soon.

Sincerely,

John McCain

Oh, him.

Please, folks, send Gary your money instead.

Labels: 2008, Health Care, Republican Party

Housecleaning: What I Missed in the Past Week while house-cleaning

This is by no means a comprehensive list.

- You Not Sneaky! dropped two great posts here and here on Malthus, Economics, and Malthusian Economics, complete with a spreadsheet model available for the download (all right, this is really two weeks ago but (1) I need something that keeps this relevant to economics and [2] I really did only find them today)

- Gary Farber is moving from Denver, CO, to Raleigh, NC. Maybe he just can't deal with Democrats. Oh, wait, there's another, much better, reason:

Why Raleigh? Enter: Amygdala Woman. (Sometimes known as "Malibu Stacy.")

Go hit the tip jar, those of you with revenues.* - There have been multiple earthquakes in Reno, but fortunately, Susan Palwick and her husband Gary are fine so far. Our best wishes to them and others, some of whom were likely not so lucky.

- Larry Niven, who is independently wealthy to the extent of having a relative of his named in a passage blind-reffing the Teapot Dome scandal in a Heinlein novel** and was responsible for Shira's last Major Fandom Event Participation,*** has gone completely bonkers (sad h/t to Dr. Black).

- Erin uses cold cream. My imagination runs wild, but not on a family blog.

- Janelle of Bond Girl Fame hasn't posted an update on the injuries on the set of the latest film, but one can understand that she has other things on her mind.

- I was expecting Rory at Eat Our Brains to respond to this post of Patrick's, but he has (instead?) decided to become a Zen Master or something, and, finally,

- Shira can rejoin SFWA (though I still need to find out who the Canadian Regional Director is).

There's probably more.

*By the way, does this mean Obama loses a delegate? Chris Wallace should ask The Annoited One-to-Be on his regularly-scheduled Fox News appearance.

**"Since Secretary of State Fall was convicted or receiving a bribe Doheny was acquitted of paying."

***Louis Wu's Birthday Party at the 1989 WorldCon in Boston

Labels: Eat Our Brains, Erin O'Brien, just life, MakingLight, sf

Glories of the Working Life (first of a series)

Ignore, for the moment, the presentation values that were quite acceptable fifteen years ago (i.e., that it looks as if it was prepared in MultiMate or WP 5.1 with Helvetica).

Note the boxed entry.

Users may also wish to examine how many of the presenting firms are still intact in their present form.

Labels: fragments of the past, High Finance, just life

Quote of the Day

Michael O'Hare:

The ease with which politicians say "gas prices are too high" combines their cowardice (or cynicism and irresponsibility, or maybe just ignorance) with a widespread confusion of price with cost in the public mind... The distinction is no piece of technical arcana, but one of the most fundamental keys to getting policy right, and in this case, a very big batch of policy with enormous consequences. If you don't understand the difference, you do what Hugo Sanchez Chavez does and suppress the price by enormous public subsidies. Unfortunately, the cost of anything is quite independent of what we want it to be, or the price at which it is offered, because cost a reality sort of thing, the value of the economic resources consumed in providing it... If you lie about the cost of gasoline, or anything, by offering it for sale at an arbitrary price, the cost doesn't change, but the behavior of everyone gets crazy with very bad consequences.(A related rant may be forthcoming, assuming I have time to write it later.)

Two Questions on Economic Growth in Developing Countries

- If the prescription for open markets and universal trade used by many of the "Washington Consensus" is accurate, can someone please cite two examples (I'd probably settle for one, but it would have to be a Really Good One) of companies that have made the transition using that method?

- Relatedly, how is a country supposed to develop a Competitive Advantage in such a scenario?

Cross-posted at Economics Question of the Day.

Labels: Economic Development, free riders, free trade

Sunday, April 27, 2008

How Not to Pack (third in a series)

Unintentional Non Sequitur of the Day?

Shira: "I got some boxes from Whole Foods. Most of them held Febreze, but they smell really bad."

Labels: just life, My home not native land

While Tom Creates Serious Posts, I compare Instapundit reactions

I'm traveling Nostalgia Lanes recently, between cleaning out files and documents and some strange links in my e-mail. So let's Go to the Movies!

Robert Redford's Lions for Lambs averaged $3,025 per theater on its opening weekend in 2007.

Instapundit was loud and clear, twice, once directly:

"Lions for Lambs' Could Lose $25 Million." One can only hope.

and once while pillorying Redacted:

Lions for Lambs isn't exactly raking it in, either.

(I personally prefer this Google Advanced Search link, where the professor opened the week by wondering "IS THE DOLLAR TOO LOW? Or is the Euro too high?" linking to someone in the Torygraph who bemoans:

The die is now cast. As the euro brushes $1.50 against the dollar, it is already too late to stop the eurozone hurtling into a full-fledged economic and political crisis.

13+% later, we're still waiting for that European crisis.)

Now, Expelled, the selfmockumentary starring Ben Stein, opened wide and grossed $2,824 per theater opening weekend (nearly 7% less).

So what did we get?

I HAVEN'T SEEN BEN STEIN'S EXPELLED, and I regard "Intelligent Design" theory as pernicious twaddle. But it's interesting to see Stein clobbering Morgan Spurlock in box office. At any rate, according to the comments, at least, there's more to the film than I.D. twaddle.

Insty links,of course, to the Liberty Film people, who in turn link to a site that simply lies outright:

One notable success has been the intelligent design documentary Expelled: No Intelligence Allowed, featuring Ben Stein. Released on a little over 1,000 screens by the small Christian-based Rocky Mountain Pictures, the film picked up another $1.03 million on Saturday, and it will finish the weekend with just under $3 million. Not bad for a movie shot on a shoestring, released by a virtually unknown distributor and promoted very lightly.

Give you a hint: if you release on over 1,000 screens, you didn't "promote very lightly." Unless you bribed a lot of theater owners.

Labels: intelligent design, movies, PortfolioMarketMovers

Thursday, April 24, 2008

How I Spent Earth Day 2008

I had the rare experience of riding along one of the marvels of modern railway engineering, the Union Pacific's main line in Nebraska, over which some 400 million tons of coal from the South Powder River Basin in Wyoming (and plenty of other freight) travel over three and four tracks to a power plant near you. Stephen Karlson calls it the "world's finest railroad," not at all unjustifiably considering that these 20,000-gross-ton coal unit trains and dozens more like them every day move at astonishingly low costs per ton-mile. (It doesn't hurt that the coal is, for the most part, rolling gently downhill.)

Seeing all this coal does slap one in the face with the magnitude of any significant transition away from coal-burning for electricity generation. If nothing else, any major reduction in coal shipments to U.S. power plants in the near term would probably just be offset by export volume.

Labels: Energy, Trains Planes and Automobiles

Wednesday, April 23, 2008

Rush Knows His Audience

I'm buried right now, even without working for direct pay, but want to make certain this gets mentioned.

Mark Duggan and Fiona Scott Morton have an NBER paper (#13917; gated link here*) examining the results of the first year of Medicare Part D. To no one's great surprise, they find

But what is most (generally) interesting is the list of most common drugs prescribed under Part D:

Lipitor, Zocor, Prevacid, Nexium, Zoloft, Epogen, Celebrex, Zyprexa, Neurontin, Procrit, Effexor, Advair, Paxil, Norvasc, Pravachol, Plavix, Allegra, Wellbutrin, Oxycontin, Fosamax, Vioxx, Singulair, Protonix, Actos, Ortho, Aciphex

That's right; "hillbilly heroin" is #19 on the IMS Health list of prescribed drugs under Part D.

*If anyone finds a non-gated version, feel free to ref it in comments and I'll add it. (Tom, just edit appropriately if you find one.)

**Duggan and Scott Morton do note that "If a price is suboptimally high, there can be over-utilization of the treatment, with physicians and other health care providers potentially inducing the demand of consumers," but appear to assume that is not the case here.

Labels: Bushonomics, Economics, Health Care

Tuesday, April 22, 2008

The New Hometown will play the Old Hometown

Krugman admits Jeremy is smarter than us

Note the progression here:

The essential story there was one of hard-science arrogance: Forrester, an eminent professor of engineering, decided to try his hand at economics, and basically said, “I’m going to do economics with equations! And run them on a computer! I’m sure those stupid economists have never thought of that!” And he didn’t walk over to the east side of campus to ask whether, in fact, any economists ever had thought of that, and what they had learned. (Economists tend to do the same thing to sociologists and political scientists. The general rule to remember is that if some discipline seems less developed than your own, it’s probably not because the researchers aren’t as smart as you are, it’s because the subject is harder.) [italic his; emphasis mine]

Labels: Economics, Social Science

Preparation to Move: They Fight Differently in Canadian Hockey Games

Finally, a hockey fight video I can embed on a family blog. This is the way it should be done:

Labels: hockey, My home not native land

Friday, April 18, 2008

Multiplication of Entities

That Obama's "bitter" remark is substantively wrong has evidently reached a height of liberal-opinion fashion. [*] I even agree that the partisan shift of the former Confederacy explains much of the Republican ascendancy. But would someone please then explain to me the ascendancy of God, guns, and gays politics? What do Karl Rove and minions not know that they think they know? Or, if it's just a new encoding of the "southern strategy"'s appeal to southern racism, why is it needed (or more effective)?

[*] I'd say "the," but Krugman's pronouncements are not so infallible when he's on the Clinton-v.-Obama beat.

Labels: ObamaNation, Politics

Welcome Isthmus Readers

Here's Overture Center Finances: A Fine Mess.

Everyone else, here's Tom Laskin's The Overture Center: Coming up short, reviewing the financial crisis at Madison's arts facility.

Labels: Madison

A Reason I'm Not Expecting Cheap Oil Soon

A growing market, Chinese nouveaux riches tooling around in Audi SUVs (AutoWeek):

The other big debut [at Auto China 2008], the Audi Q5 crossover, hasn't had any exposure, so its premiere will be closely watched. Audi is using the Beijing show to roll out its newest model in part because it sees China as a key market for growing sales. China is now Audi's second-biggest market, after Germany.

Labels: Energy, Trains Planes and Automobiles

Thursday, April 17, 2008

How Not to Pack (second in a series)

When culling the CD collection, do not leave "How Come" from D12 World on the stereo when the three-year-old comes in from playing.

Labels: just life, My home not native land, pop music

Wednesday, April 16, 2008

Back to Normal: Do It with Mirrors, John?

After I tried (with a hint of irony) to say something nice about RWR (and Tom corrected me*), John McCain undermines all that goodwill with another mailing:

While many of us are aggravated and displeased when we see exactly how much of our hard-earned money goes to the federal government - if one of my Democratic opponents is elected in November, you can be certain your tax rate will increase across the board. [emphasis his]

Hmmm; increasing deficits (ameliorated only slightly by a Social Security Trust Fund surplus that even Andrew Samwick is now defending), an ever-more-costly war (some of which is "off balance sheet" [think derivatives], so the actual deficit is ever higher), and more than a 2% difference between income (read: taxes) and outflows that have increased at greater than the rate of inflation only for defense for all of the Discretionary Spending. (And if cactus at AngryBear updates this post,*** I suspect the differences will be even worse.)

But I'll hold out hope, John; after all, you're a Straight Talker. What's your plan?

I believe today, as I have always believed, in small government, fiscal discipline and low taxes. I believe that tax cuts work best when accompanied by lower spending. And I make the promise to you that if elected president, I plan to make the present tax cuts permanent, lower corporate rates from 35% to 25% and end the Alternative Minimum Tax, which will affect millions of middle class families.

Let's see:

- "make the present tax cuts permanent": I assume this means the 2001 and 2003 cuts that were scheduled to "sunset" in ten years because even then—with a trend toward paying off deficits and Saint Alan talking about the Evil that would be a Sovereign Wealth Fund—our representatives and Senators knew they would be too costly on an Infinite (or even Extended) Time Horizon. So monies that are in the baseline CBO projection, for instance, would not be there. Need taxes, or cuts in spending.

- lower corporate rates from 35% to 25%: Well, as pgl pointed out last year, it would be absurd to assume that the actual corporate tax rate is at 35% now.**** But, once again, baseline projection monies are no longer there. Need taxes, or cuts in spending.

- "end the Alternative Minimum Tax"—this is the first year in a few that I wasn't hit by the AMT. But this is also, definitionally, the first time in a few years that our Gross Income was less than about 250% of the national average. And this is outright elimination. (The CBO released a report this month [PDF] that projects the 10-year cost of just indexing the AMT to inflation of $700B.) So this is a major loss of revenue, without any noticeable income

So that's three proposals: all tax cuts without a single revenue source in sight. And I'm not betting that John "we'll spend 100 years in Iraq, but don't worry, only 95 of them will be as an active fighting force" McCain is going to reverse the GWB trend in increasing defense spending at greater-than-inflation rates.

The kicker? There's only one way to cause this miracle to happen:

But I cannot succeed in my efforts without your immediate financial support. [I spare you the link]

So the only way not to pay taxes is to pay tribute to a man who plans to increase deficits in a major way, crowding out entrepreneurial activity and further impairing growth.

Makes me long for the days when RR appointed David Stockman to run the OMB. At least then we got Straight Talk from a Republican.

*This may be what I get from believing my accountant, who may well have confused 1986 and 1996.** Though it remains remotely possible that Reagan did start the ball rolling to some small extent:

Most Americans already escape the tax by either rolling over, or deferring, their capital gain when they buy a more expensive house, or by taking a one-time exemption for up to $125,000 in gains allowed for those 55 and older.

So it's possible that Reagan initiated it, while Clinton both eliminated the age restriction and raised the limit. But that's probably not the way to bet.

**We are both of an age where that happens. Having heard the, er, update of Kurtis Blow's classic "Basketball" last weekend on Radio Disney, I suggest that the decay of memory and the "memory of decay" is natural.

***I thought he had, but I can't find it on a quick use of The Google (TM Sadly No!).

****If we do the math, taking the 39.3% overall corporate tax rate here and the proportions documented by the CBO here***** [PDF; 1.6% of GDP for Federal; 2.1% for all], we would conclude that the effective Federal corporate tax rate is currently 39.3% * 1.6/2.1 or 29.9%. So take heart, John; we're halfway there and you haven't done anything yet.

****I am comparing a 2004 ratio with 2006 data, but since the Tax Foundation indicates a difference of 0.1% between 2001 and 2006, this does not seem unreasonable.

Labels: Bushonomics, defense, deficit, Personal Finance Advice of Alan Greenspan, Republican Party

Back to the AEA

My favorite paper from this year's AEA is now available from NBER (gated; non-gated copy available here).

Also noted, the prepared text for the most interesting presentation (most interesting, to some extent, from the non-prepared text at the beginning) was the lead article in the current issue of

More later, which probably means the middle of next week.

Labels: Bushonomics, Economic Development, Economics

At Least We Can't Be Too Stupid

Seeing how John McCain's crack (smoking) economic team managed to fool Our Ever-Sharp Media as to the magnitude of the federal gas tax (correct answer: 18.4 cents), I have to ask the question — feature or bug? For McCain, I have no idea. For the economy at least, at times like these the low gas tax becomes a crypto-feature because Politicians of Great Integrity who Wisely Love the Free Market except when the market has to be counteracted for political purposes can only make St. Greg de Pigou cry so much. Same goes for such local initiatives as may arise related to the modestly higher state taxes. Ultimately, the political answer may be, why bother if nobody will notice.

Obviously, it would have been a good idea to have funded the transition from the drive-anywhere-for-anything economy before Peak Oil struck, but the best policy (going along with the principle that the Fed should do its bit to accommodate the needed expenditures) would be better late than never.

Labels: Pigouvian tax

Tuesday, April 15, 2008

Taxing the Data

I'm sure that many, many bloggers have offered their opinions on the likely consequences of the economic stimulus package for the economy. I don't have anything to add here, nor to I wish to trivialize the very real impact the recession is having on people's lives and livelihoods. But, I can't help but speculating about the consequences of the economic stimulus package on the livelihoods of number crunchers everywhere.

Unpack.

It's expected that roughly 20 million "extra" returns will be filed this year, out of a baseline of roughly 141 million returns. Most of the increase is likely to come from retirees whose income is too low for them to bother filing a return in a normal year. These additional returns at the bottom of the income distribution are sufficiently numerous to affect most inequality measures (except the 90:50 ratio).

The Great Data Swami predicts that as soon as the IRS data from 2007 are released, there will be glut of journalistic and quasi-journalistic social science articles pointing out the dramatic increase in levels of income inequality in 2007 relative to 2006.[1]

Within moments, left-leaning politicians will decry the accelerating pace of change in the gap between the haves and the have-nots. Paul Krugman will become a household name even outside the Times-select-reading elite.

Mere sound-bites later, right-leaning politicians will (a) claim that inequality statistics from the 2007 tax year are meaningless; (b) advocate for tightening the restrictions on the release of aggregate statistics from tax data, on the grounds such statistics violate Americans' unassailable [2] right to privacy; and (c) proclaim that research on income inequality is as wasteful of government funds as, well, research on gender or race. Those of us who study income inequality will no longer be able to use the words "income", "inequality", or "gini" in our proposal titles.

And with that, I'm off to put the finishing touches on my tax return.

[1] All of this assumes that the annual IRS data do not adjust for non-filers in their income estimates, or at least do not do so with much accuracy. Truth be told, I'm a CPS/SIPP gal myself, and have never used the IRS tax return data. If anyone less lazy than me knows more details about the IRS data, I'm all ears. Well, eyes, at least.

[2] Except for that whole wire-tapping homeland security bit.

Labels: Income Inequality, Tax Incentives

On Tax Day, I Say Something Nice About Ronald Wilson Reagan

UPDATE: See correction from Tom in comments. Oh well.

Reagan defenders are perpetually saying that, after he created massive deficits and a recession with the 1981 tax cuts, his people learned better, and all of the following tax cuts were "revenue-neutral."

I'll leave it to the folks at AngryBear to graph out the truth of that statement; suffice to say, the 1986 revision (discussed here and, most especially, here, to pick two from Divorced One Like Bush) has long been cursed by me. Generally, 1986 made it harder to get out of a poverty trap, and easier to maintain Generational Wealth without doing anything.*

But—or, probably, for example—the one thing that 1986 did was eliminate the first $250,000 per person on gains from the sale of real property.** And since there is no chance we will make anything near that limit, there is no chance that I will have to negotiate with the IRS over why we haven't didn't buy another house in the United States over the following two years.****

And, in part, we have RR to thank for it.

*If you believe either of those two is a good idea, please explain your theory of economic growth, and Why No One Will Publish It Except the AEI.

**Technically, I believe the ceiling was set lower, and raised either seven or ten years later.*** But Reagan set the standard for considering basic housing to be "an investment."

***Strangely, those try to cast some portion of the blame for the housing boom/bust on that Clinton administration action ignore that the standard was set by Their Leader.

****This, of course, assumes the current house can be sold.

Labels: Housing Bubble, mortgage, My home not native land, Tax Incentives

The Bad Penny

Were it not for D-squared, I'd have to wonder how Xavier Gabaix and Augustin Landier managed to get published in the QJE and not the American Enterprise Institute working paper series. So it's maybe more a matter of a disappointing reminder that the peer-review system is the worst one apart from all the rest than a call to the barricades to see the NYT maintain its death spiral in part by telling me that Gabaix is shilling his and Landier's dubious little result on executive pay in the AEI house organ (without notifying me that it is the AEI house organ we're talking about).

The verdict from two years ago was that they derived some mildly interesting results from fantasy premises, starting with the idea that the CEO labor market is frictionless and neoclassical. From some perspectives on economics research methods — and sometimes to the annoyance of economics critics — that can be a feature and not a bug; it's a common research method to characterize how far reality departs from such flights of fancy. The problem here is that even The American's Laura Vanderkam can't help but recount a variety of gross features of executive pay (the heads-I-win, tails-you-lose arrangements, the divergence in compensation between the executive ranks and everyone else, the non-observability of talent, the factoid that investor willingness to pay more money for a dollar of earnings is a major driver of recent market cap increases) that are puzzles for if not grossly inconsistent with a model of a frictionless CEO labor market.

Anyway, the Davies model seems to me to be a rounder peg for this particular hole: economists of a couple generations ago did their duty by providing a plausible explanation why corporate executives were underpaid, certain frictions in the system did their bit, and belatedly-discovered holes in the theory have been non-neoclassically slow to be plugged.

Labels: Economics, The New Gilded Age

Monday, April 14, 2008

In Other Good News

Peak Oil goes to Russia. Hey, and I was pretty close to $2/day in fuel savings from the bike commute as things stood.

As a microeconomist, I'm perhaps less inclined than some you'll read to wring my hands over the Fed's possible softness on commodity-price inflation. We occasionally get the notion that increasing prices for some goods should be interpreted as a signal to consume substitutes in greater quantities. You might indeed wonder if trying to reduce the price of oil through means that involve throwing millions of people out of work is a worthwhile Fed initiative.

"Good Faith": NBA speak for double-cross

Having been in Charlotte shortly after an owner blew up his team and treated the city with contempt—followed by city officials bending over further and saying "Yes, please, wherever and however you want"—this is not a surprise:

NBA commissioner David Stern says he is convinced Bennett made a good-faith effort to keep the team in Seattle.

Bennett and ownership partners Aubrey McClendon and Tom Ward exchanged e-mails in April 2007 in which they discussed whether there was any way to avoid further "lame duck" seasons in Seattle before the team could be relocated.

Bennett, who had promised to negotiate with Seattle for a full year before deciding whether to move the Sonics, responded: "I am a man possessed! Will do everything we can. Thanks for hanging with me boys."

When Seattle gets their new expansion team, the appropriate track will come from the final Nirvana studio album. As this remains a family blog, here's a YouTube link. The former mayor of Charlotte can teach you the song; she sang it very well. And the results are impressive; good thing for them the Knicks are still in the league.

Labels: Giffen Good, pop music, sports

Not A Good Sign for High-End Housing

Most of Madison was never especially bubbly, but the Big Shitpile has a way of getting under one's shoes:

So no high-end housing market recovery until at least the fall. Now that buyers of $10,000 fridges demonstrably are not recession-proof, we may need to look to mega-yacht cancellations for more bearish news.Sub-Zero/Wolf of Fitchburg, a manufacturer of high-end refrigeration and cooking appliances, will lay off 235 employees at its plants in Fitchburg and Phoenix, Ariz..."It's no secret what's going on in the economy and what's happening with consumer confidence," [Chuck Verri, VP of HR] said. "We're building inventories too rapidly and we've got to do something to react."

Verri said employees were notified Monday and will lose their jobs on or after June 13.

He said the slowdown in construction of high-end homes and condominiums is a major factor in the layoffs.

Labels: Housing Bubble, Madison

Saturday, April 12, 2008

Choose You Own Adventure: How Not to Pack (first of a, likely, series)

You have three boxes. One is large, but has a very weak bottom. The other two are smaller and stable.

You pack the large, unstable box with (mostly children's) books, but are careful not to fill it to the top.

You attempt to carry the box of books down the stairs.

Do you:

- watch in horror as the books fall from the bottom early in your journey?

- make it to the turn in the stairs and end up in the hospital?

- realize immediately what will happen and move the other two boxes, leaving the large one for the next

victimperson?

Fortunately, in this case, the answer is (1).

Labels: just life, My home not native land

A Plea to the Blogsphere

If you're going to read people (such as David Brooks) so I don't have to, could the excerpts please be shorter??

Five years? My brain hurts, a lot.

Labels: blogging, Brad DeLong, Journamalism, Meta

Friday, April 11, 2008

Retail Concepts the World Never Asked For

Electronista: Microsoft exploring Apple-like retail shops?

Alleged sources near Microsoft say that the company hopes to boost its brand by launching a retail chain that presents an ideal Microsoft experience... [emphasis added]

...added, I'm clearly slipping as I almost forgot that the story broke late last year.

Labels: Modern Retailing

Overture Center Finances: A Fine Mess

Quick background: The Overture Center, Madison's $205 million concert hall and arts center, was a gift from local philanthropist Jerry Frautschi (who made his fortune investing in American Girl, founded by his wife and sold for big $$ to Mattel). The gift was structured so that about half was put in a trust fund, intended to pay off construction debt and contribute to the Center's maintenance, assuming it made roughly 9% annual returns off stock market investments. The year was 1999. D'ohh!

After years of 2% annual returns, the trust fund represented insufficient collateral for the bankers, so a refinancing plan was hatched, and approved in late 2005, that required the City of Madison to guarantee a portion of the debt. The plan would work just great as long as it attained an 8.25% annual average return and the trust balance stayed over $104 million. That also hasn't worked out so well, as noted here a week-and-a-half ago.

My question has been, how have the Overture trust fund's managers managed to screw up so badly? Well, other than the obvious reason that 8.25% is well above any sane person's idea of a risk-free return. Courtesy of Isthmus executive editor Marc Eisen, I've seen a spreadsheet with a summary of the Overture trust's investments, and can only conclude that the investment choices never gave them a serious chance. For junkies of mid-sized institutional asset management stories, some gruesome details are after the jump.

I'd divide the trust fund's management into two eras, the Cash Era and the Alternative Investments Era.

The Cash Era ran from late 2005 to late 2006. The trust fund's balance ranged from $106.2 million to $109.3 million over the period, and 46% to 61% of that was held in "cash equivalents." The balance was in "general equities" (which I take to be meant generically, and not the firm General Equities) and Fairfield Sentry Ltd., a hedge fund. The higher cash percentage was sustained for the latter two-thirds of the year, when the trust turned a good portion of its Fairfield Sentry holdings into cash equivalents. My naive calculation from the spreasheet says that the equitites returned 4.6% and the Fairfield Sentry fund returned 8%. In 2006, you could have made right around 5% with a very good money market fund, such as the institutional share class for Vanguard's Prime Money Market fund. The upshot was that their weighted average return was right around 5% for the year. With that asset weighting, the trust had to make 12.7% off the non-cash-equivalent assets to reach the 8.25% target. 2006 actually was a good year for stocks — Vanguard's Total Stock Market index fund returned north of 15%. They chose a bad year not to be 'seeking beta.'

The interesting question is why they stayed in cash for so long post-refinancing. Pardon me for thinking that the financial geniuses behind the refinancing might have had an investment plan ready to roll upon approval. None of the obvious answers — they didn't have a plan, the Cash Era represents an inept plan, and they chose a deliberately defensive position to avoid the political embarrassment of a quick I-told-you-so from refinancing opponents — is confidence-inspiring.

The Cash Era ended in late-2006, as the cash-equivalents gradually moved into a series of other investments. At the end of the series I've seen (3/14/08), only 2% of the Overture trust is held in cash equivalents. I call this the Alternative Investment era as it was kicked off with a roughly $15M investment in "Highbridge Fund," which appears from the value of holdings to be the quasi-hedgey Highbridge Statistical Market Neutral fund (as of 3/14, 21% of the fund's holdings). Stakes in Pimco All Asset fund (a fund of Pimco funds, 16%), principal protected notes (PPNs) from JPMorgan and Barclay's (the latter purchased with the proceeds of the "general equities,"14% and 8%, respectively), additional investment in Fairfield Sentry (18%), and "JPMorgan muni's" (20%) followed.

It's hard to reliably track performance across the board because of apparent asset sales and purchases, but nothing has come especially close to putting in an 8.25% return over the period. The highest-flyers, the Fairfield and Pimco funds, have had 1-year returns around 6%. The Highbridge 1-year return was 1.2% (they've done relatively well YTD), the munis are up 2% over the 7-month period they've been held, and the PPNs down. The upshot is that the trust is showing a weighted average return around 3% for the last year, far below the target. Granted, all I need to do is look at my 401(k) performance to see that it's been a tough year through the end of March — I'm down 3.3%, though then again my five-year average is 9.7%. An irony is that while Madison Cultural Arts District Treasurer told the Cap Times that it would be "a very unfortunate change" if the creditors forced the assets into Treasury securities, which might be true now, had they actually been in Treasurys all along, they'd have ridden the bond market's flight to quality well past their return goal for the past year. Whatever the skills of the MCAD, investment timing ain't it.

The better question, perhaps, is what the prospects would be for this asset mix to earn 8.25% on average in the future. The underlying assets for the PPNs could be anything, so it's hard to say there. The munis won't under foreseeable interest rate environments. Pimco All Asset seems to be tuned to produce single-digit annual returns. Highbridge hasn't exactly been minting 'alpha,' and who knows about Fairfield Sentry. If the PPN investments were selected at least for perceived safety before the fact (actual performance notwithstanding), then I'd have to say it isn't going to happen. If nothing else, the MCAD seems to have done a good job of picking relatively high-cost holdings, which just increases the return that has to be earned from the underlying assets for the trust to net 8.25%.

This brings me back to my main point — the MCAD is undercapitalized, and they should get cracking on raising money. That was something that was supposed to have been facilitated by keeping the facility in the hands of the MCAD instead of under direct city ownership, but a capital campaign seems to have become a priority only now that they're in the soup. If they want to make good on the facility's promises, and shut us critics of their financing misadventures up, they need to raise a lot.

Return to the Marginal Utility main page.

Labels: hedge funds, High Finance, Madison

Thursday, April 10, 2008

Time to Brush Up On My Newspeak

This morning was a test of how many times I could hear the word "pause" used on NPR, without someone translating the usage into standard English, without going (more) insane. The answer is a lot, but not so much as to make it safe for me to listen to Morning Edition all the way through.

Let's just all say it: a "pause" in the draw-down from the "surge" means that the "surge" is a "(quasi-)permanent escalation."

Labels: Iraq

Wednesday, April 09, 2008

My Favorite John Updike Novel Needs to be Rewritten?

Scott Horton discovers that the guys at G-Mu (not these guys; the historians) have dropped James Buchanan to #2 in the Pantheon.

Memories of the Ford Administration (even though it elides Buchanan's homosexuality) may never be read the same again.

Labels: Bushonomics, History, literature

Tuesday, April 08, 2008

Why I Love the Blogsphere

Consider this the counterpoint to yesterday's "they played without me" post.

Every once in a while, there is a statement that is so egregiously offensively wrong that it demands a blogspot. But, since after today I have something in common with Barkley Rosser's eldest daughter, I'm buried.

Fortunately, Felix came through with bells on.*

The statement, by the way, is:

Some argue that adjustable rate mortgage (ARM) originations fueled the bubble. Yet the ARM's share of total originations is a very weak forecaster of home prices, implying ARMs, although a source of cheap financing, are not a determinant of home prices. If ARMs were not available from 2001 to 2004, home purchases presumably would have been financed with long term debt, which was also very affordable.

You can guess the source.

*The only thing he leaves out is that Alan Greenspan himself encouraged people to take out ARMs, just as he started tightening. Of course, as with Himself being 100% in bonds (at his age) in 1996, just before he started loosening, this is purely coincident.

Labels: Housing Bubble, mortgage, Personal Finance Advice of Alan Greenspan, PortfolioMarketMovers

Dep't of Moon Shots

My prediction of the day (which has a less-specific timetable for achievement or failure than, say, Dow 36,000):

Even though it was a bullshit non-initiative initiative of the Bush Administration, the 'hydrogen economy' will prove to be a far less stupid idea than the biofuels economy.

Reference: Brad DeLong at Project Syndicate (h/t PGL at AB), saying this, which I think is wrong:

The first locomotive ["heavy investment in information technology"], however, ran out of fuel seven years ago, and there is no clear technology-driven alternative leading sector, like biotechnology, that can inspire similar exuberance, rational or otherwise.This is wrong, in part, because nearly every sunbelt building's roof is just sitting in the sun like a dope.

Labels: Energy

Monday, April 07, 2008

I Stop Reading Blogs for a Couple of Days

And the Really Cool Discussions pass me by. (Which is as it should be.)

Fortunately, YouNotSneaky! has my (and your) back. And adds value, increasing returns with:

Socrates thought there were two, maybe three, kinds of people in the world and that you could arrange them in a hierarchy;

1. Those who don't know but think they know.

2. Those who don't know but know they don't know.

and then maybe some lucky ones;

3. Those who know and know they know.

There aren't many people in the 3rd category. But for some reason we always expect our models to move us from the 2nd category to the 3rd. And we're not satisfied if the movement is from the 1st to the 2nd.

and it gets better (and easier to understand, even without the artifice of order) from there.

Labels: Economic Development

The Last Worthwhile Part of the Old Firm is to be Destroyed

Even Jimmy Cayne didn't screw this one up, but Jamie Dimon plans to ruin the one Unarguably Good Thing they did:

JPMorgan Chase...wants to dismantle the firm's jobs program for people with disabilities, according to sources familiar with the matter.

That means about 40 Bear workers with disabilities who were given jobs at the firm over the years will likely be laid off.

These are the workers one would see every day, working hard and getting their jobs done. Many of them long predate my first time there, in the early 1990s.

And none of them ever made thousands or millions or even billions of dollars of shareholder value go away.

Stick a fork in it; one way or another, Bear Stearns is gone.

Labels: The New Gilded Age, The Old Firm

There is a G-d?

And maybe Alanis Morissette portrayed her accurately, judging by the current contretemps at the Mortgage Bankers Association (h/t Dealbreaker).

Economists Question: Identify the "moral hazard," if any, in the linked story. Explain how it could have been quantified, mitigated, or defined by one or both of the parties.

If you do not believe there is "moral hazard" in the above case, but still believe in "moral hazard" for residential transactions, please define the differences so as to explain the differences between the two scenarios.

Labels: Housing Bubble, humor, Moral Hazard, mortgage

Friday, April 04, 2008

Even Worse Than It Looks?

If someone wanted to make the argument to me that the CES Net Birth/Death Model is more trouble than it's worth, today would be a good day to do so.

The U.S. employment report for March, as most of you probably know, stank. But it would have stank more but for this model, which estimated that there were an additional 28,000 jobs in the construction sector, 7,000 in manufacturing, and 6,000 in financial activities jobs. I don't think so.

One of the things that keeps applied economists busy is figuring out whether Sophistimacated Methods are better than simpler ones. In this case the model seems to perform worst exactly at the turns in the business cycle when you'd think policy-makers would want the most accurate reading on employment changes, which is not a great recommendation.

Thursday, April 03, 2008

Why I hate April Fool's Jokes

Via Tim F. at Balloon Juice.

(link statements too painful for me to quote; Tim F. did here.)

Labels: Bushonomics, policy wonk, Science

If anyone cares, we Scored 17.4%

Which is absurd, in context.

And the addition, "This is 149% MORE than other websites who took this test," belies reality.

When Lee Papa can't even break 50%, they must be using a log scale.

But our reputation as a "family blog" is endangered, so I promise not to mention Christopher Cox for the rest of the week.

In the Meantime, We are Reminded what the phrase "Representative Government" Means

I'm watching (mercifully, with the sound off) Christopher Cox (R-CA; patronage job as SEC Chairman), if CNBC is correct, blatantly lie to Congress (CNBC Chyron: "What happened to Bear Stearns was unprecedented" Let's see: a major financial player with large bets in a specific market sector gets caught ignoring the rule "The market can stay irrational longer than you can stay liquid." Where have we heard that before?) and figuring that Yves or Steve Randy Waldman will take care of it so I don't have to.

And I start fearing for the democratic process, because seeing Christopher Cox explaining financial markets as if he knows anything about them other than how to provide patronage is scary.

So it is reassuring to see this piece on Political Radar, as a reminder of that vox populi does, occasionally, work:

In the Senate this week, a bipartisan bill to help stem the tide of foreclosures nationwide is sliding through the senate like water on Teflon.

A similar bill fell prey to partisan bickering at the end of February when Republicans blocked it after Democrats refused to allow unrelated amendments.

What happened between then and now to end the partisanship? Vacation. That's what. Because while most people take vacation to forget about their jobs, in Congress they take vacation to go talk to their bosses, the people.

"I suspect the other major event was the fact we went home for a couple of weeks. Nothing like going home, Mr.. president, to get a message," said Sen. Chris Dodd, the chairman of the Senate Banking Committee, who engineered the bipartisan bill in a marathon 20 hour bipartisan brainstorming session with Sen. Richard Shelby, R-Ala....

"But they asked the legitimate question, if it was good enough for people to get together to solve a problem on Wall Street, what about the problem on my street? What are you doing here to see to it I can stay in my home? That our neighborhood will not collapse? That our taxes and properties and neighborhoods will not further deteriorate? I suspect more than anything else, going homemade a big difference and -- going home made a big difference."

In the world of economists, this will probably be seen as an inefficient solution, encouraging the (mythical) Moral Hazard.

But in the real world, Congress has ready access to Wall Street bailout advocates. It's only on vacation that they speak with the people who elect them.

It appears that Gore Vidal is correct that the Congressional offices and buildings should never have been fitted with air conditioning: not because of the mischief-making, but rather because it reduces the chance of their getting actual voter input.

Labels: Democracy, High Finance, Moral Hazard, Regulation, The Old Firm

Wednesday, April 02, 2008

Even I'm Not that Gullible

Metro reported yesterday that CBS's Les Moonves was so impressed by Britney Spears's appearance on How I Met Your Mother that they decided to make her the centerpiece of a show—a remake of the Mary Tyler Moore Show.

It wasn't until I read the link at this post from Steve Gould of EoB that I realized that yesterday was more than the traditional birthday of our cat.*

So I'm gullible. But even I'm not as gullible enough to believe the claim of Lehmann's CEO today that he has evidence that hedge funds "conspired" to destroy Bear Stearns by short-selling.

It's not that I don't believe multiple hedge funds shorted the firm, or even that some of them spoke with each other. But the conversation was more likely,"Are you short BSC?" "Better believe it. You too?" "Of course." than some clandestine activity.

Let's be clear: when your firm is leveraged over 30x itself, when most of your revenues come from an area that hasn't generated enough volume to support your structure in over a year (even after two major rounds of layoffs), and when your swap spreads blow out by a factor of 15 or 20 in the course of a few weeks, short sellers (who have to risk a lot more capital than derivatives traders) are the least of your concerns. Or just the icing on the cake.

Mark Gilbert mostly gets it right here:

U.S. and U.K. regulators are wasting their time threatening traders who profit from speculation about the deteriorating health of the financial community. The gossips aren't to blame for the demise of Bear Stearns Cos., and they won't be at fault when the next firm goes bang, either.

Brokers, futures traders, collateral managers and compliance officers are ranking their counterparties from strongest to weakest, and choosing to stop doing business with whichever company comes bottom. If the same name gets crossed out on every list, it spells game over for the loser -- deserved or not.

And, to be clear, when you have done Jack about it in the month leading up to the day before Ben Bernanke decides he needs to help you because no one else will, two dollars a share is for the other shareholders; getting punched out in the gym (note the correction at 7:53a.m. on 3/28) is Getting Off Easy.

But the seeds of Alan Schwartz's destruction-by-inaction were, as Gilbert notes, planted in 1998:

In his 2001 book When Genius Failed, Roger Lowenstein details the Fed's crucial 1998 meeting to convince Wall Street that it should shoulder the financial burden of keeping Long-Term Capital Management LP afloat or risk financial meltdown.

James Cayne, the CEO of Bear Stearns, told his peers—including Philip Purcell of Morgan Stanley and Herbert Allison of Merrill Lynch—that his company wouldn't join the 14 securities firms paying for the rescue.

"In unison, the CEOs demanded an explanation," Lowenstein writes. "This only made Cayne more resolute. Bear had enough exposure as a clearing agent, Cayne said. He wouldn't say more. Suddenly these paragons of individual enterprise seethed with communitarian fervor. Purcell of Morgan Stanley turned beet red. He fumed, 'It's not acceptable that a major Wall Street firm isn't participating!' It was as if Bear were breaking a silent code; it would pay a price in the future, Allison vowed."

Only the Stevens Levitt and Dubner might be surprised by that reaction. The rest of us noticed that, when rumors of an illiquid Lehmann started spreading, the first thing that happened was that Goldman Sachs trotted out a Senior Executive to confirm that they view Lehmann as (something like) "a strong, viable competitor."

When rumors started about Bear, there was about three days of silence, followed by the negotiations of March 14-16 to avoid Chapter 11 on the 17th.

That may be a case of revenge being a dish best served cold. Maybe the calls were made and no one was willing to do what Goldman did for Lehmann.

But all of the other evidence is that upper management just didn't realise that its job isn't to manage departments so much as to manage public perception by making certain that anything that might worry investors—say, the market for your CDS swap spreads going well past junk levels—is handled quickly and publicly.

That's why they pay the CEO—and the Board of Directors—the big bucks and bigger stock options. In early March, several "leaders" of BSC proved they were overpriced.

*No picture, in keeping with this plea.

Labels: hedge funds, High Finance, leverage, liquidity, The Old Firm

Why People Don't Trust Economists who talk about "The Benefits of Free Trade"

Of course, there could very well be some unemployment of workers who know only the old technology—like the original Luddites—and this unemployment will be excruciating to its victims. But workers as a whole are better off with more powerful output-producing technology available to them.

--William Easterly, The Elusive Quest for Growth, p. 54 (MIT pb, 2002)

Conspicuous by its absence is an indicator that the winners will (or should) in any way compensate the losers.*

An alternate view from one of Tom's favorite authors can be found here.

UPDATE: Pynchon presents a timeframe, which gives the lie to Easterly's claim:

But it's important to remember that the target even of the original assault of l779, like many machines of the Industrial Revolution, was not a new piece of technology. The stocking-frame had been around since 1589.

*Credit where due, he refers to them here as "victims."

Labels: Economic Development, history repeated, literature

Losing your soul may be another matter

N. Gregory Mankiw cites the current Dean of Admissions at Pravda-on-the-Chuck and comments:

"They wouldn’t write for Harvard because they thought it was a bunch of Communists, a bunch of atheists, a bunch of rich snobs, and if you went there you’d flunk out and you’d lose your soul," said William R. Fitzsimmons ’67.

Today at Harvard, it is almost impossible to flunk out.

Two of Shira's three cousins graduated Harvard: one is an astrophysicist at UCSC, the other in her residency years at UCSF Medical School.*

Good thing they didn't have to worry about failing, or they would probably be begging on the streets these days.

*The "runt of the litter" went to Oberlin, and is now writing about education for U.S. News and World Report. The slacker.

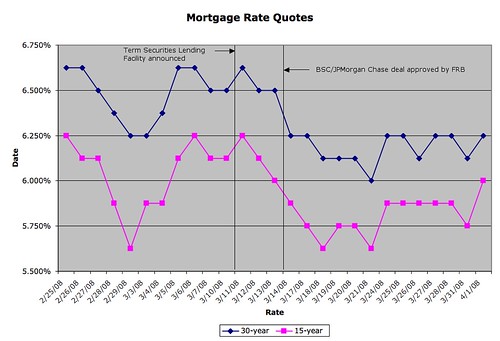

Don't Say You Didn't Get Anything From the Bailout

Here's another update to a recent post, in which I sought to figure out what was in the recent efforts by out monetary policymakers to deal with the housing troubles for me — relatively responsible borrower who still (probably) has a fair amount of home equity. Initially, the answer seemed to be Sod All, but that's changed a little, as you can see from the updated graph:

I've shown the FRB announcements of the Term Securities Lending Facility and of the approval of the BSC/JPMorgan Chase deal. Particularly after the latter, the 30-year rates (on a zero-point cash-out refi with 80% LTV) appear to have dropped around 37.5 bp from the previous range; let's call the sustained drop for someone who can afford a 15-year amortization 25 bp. So there's a little something for Main Street, though these rates aren't near the historic lows that are sometimes credited as a "fundamental" factor behind the house price run-up (in my not-so-extended family, there's at least one 15-year mortgage where the first digit of the rate is a 4).

Whether this will turn out to be worth more to the public than MBS losses flowing through the Fed to the Treasury remains to be seen.

Labels: High Finance, monetary policy, Personal Finance Advice of Alan Greenspan

Tuesday, April 01, 2008

Auto Sales Factoid!

In March, Toyota sold more Camrys (40,487) than GM sold truck-based SUVs across all of its marketing divisions.

Following up on last month's post (*), here's the latest on the divergence between crossovers market and other light truck sales for the Detroit Publicly-Traded Two. No, I'm still not going to muck through Chrysler's sales report. (**)

(*) See there for definitions.

(**) It suffices to say that theirs was miserable, too.

Labels: Trains Planes and Automobiles

For Those who come for the Legos.

Via David Pinto at Baseball Musings.

30% Down is now much harder to defend

Two months ago, with these two posts, I felt like an outlier.

Now, Menzie Chinn documents the case for 40-50%.

Labels: Econbrowser, Housing Bubble, mortgage

I Have Never Been a "real man"

But I can live with that, if Joe "I killed my intern and didn't get caught" Scarborough is calling this the standard:

Scarborough said: "You know Willie, the thing is, Americans want their president, if it's a man, to be a real man." He added, "You get 150, you're a man, or a good woman," to which Geist replied, "Out of my president, I want a 150, at least." After guest Harold Ford Jr. said that Obama's bowling showed a "humble" and "human" side to him, Scarborough replied, "A very human side? A prissy side."

(via Dr. Black)

Labels: Journamalism, just life, Politics

Some Reality Reaches Our 70 Square Miles

1. Hilldale Phase 2 delayed (again), a little sign of the CRE bust?

Barry Adams's State Journal lede blames the "harsh winter and changes to the design" for a delay in the start of construction at the seven-acre moonscape across from the office until July. This would house a greatly expanded Whole Foods, provide 3 floors of office space, and a 140-room hotel. When last we heard from Jos. Freed & Co., just a month ago, the harsh winter, the phase was supposed to be completed by spring to summer '09; it's now fall '09 to early '10.

I'd figured that Whole Foods would keep the project more-or-less on track, especially seeing as there's reportedly a tenant interested in a full floor of the office building. Oh well.

This project had been an example of the condo bust's losses looking like CRE's gains, at least for a while; the hotel replaced one proposed condo tower, and another mixed-use building (3 floors of office, eight of condos) was scaled back to a 5-story office building, since reduced to 3. Next stop, the soccer fields at Hilldale Phase 2?

2. Big Sh*tpile in Little Madison Revisited, Overture trust balance reaches new lows.

Who could have predicted that 8.25% annual returns aren't risk-free? Well, Mayor Dave Cieslewicz, of course, and the editorial pages of both papers.

The geniuses who manage the trust's investments have managed to turn $109.3M in December '05 to $100.1M as of March 14; they needed to maintain $104 million to make the 2005 refinancing work as advertised, with the trust paying the construction debt and making a contribution to the Overture Center's maintenance.

The problem has been pretty simple all along: too little money required to do too much stuff, so the plan has depended on generating returns sufficiently large that they can't be counted on all the time. As it turns out, you can be too generous and too cheap. The original assumption was a 9% annual return (in 1999, when it was assumed it would be generated from stock market holdings), and the times being what they are, they got 2% through 2005. The refinancing plan shaved off 75 bp, but was especially sensitive to low realized returns in the early years (oops).

Something I wonder is why a nonprofit endowment like this can't buy into a better class of money management. Some of you have surely seen that the peer group for Jane Mendillo, the Wellesley investment manager recently hired to helm the management of Harvard's endowment, turned in a 13.9% 5-year annual average return to the middle of last year. (I'm curious to see what the last nine months have done to the high-flying endowments.) The Overture fund isn't in this size class, but nevertheless I wonder how its management does so poorly? And why can't they just buy into the competent management of larger endowments (i.e., are there tax or regulatory obstacles to doing so)?

The solution, of course, is to raise more capital for the fund — something that was advertised as being facilitated by retaining quasi-private ownership of the facility, but which has yet to materialize except, perhaps, by way of a bailout to prevent a chorus of I-told-you-sos.

Labels: High Finance, Housing Bubble, Madison

![]()